Copart (NYSE: CPRT)

A Company that profitably grew revenues by more than 10x from $316 Mn since 2002 and grew market cap from $800 Mn to more than $28 Bn

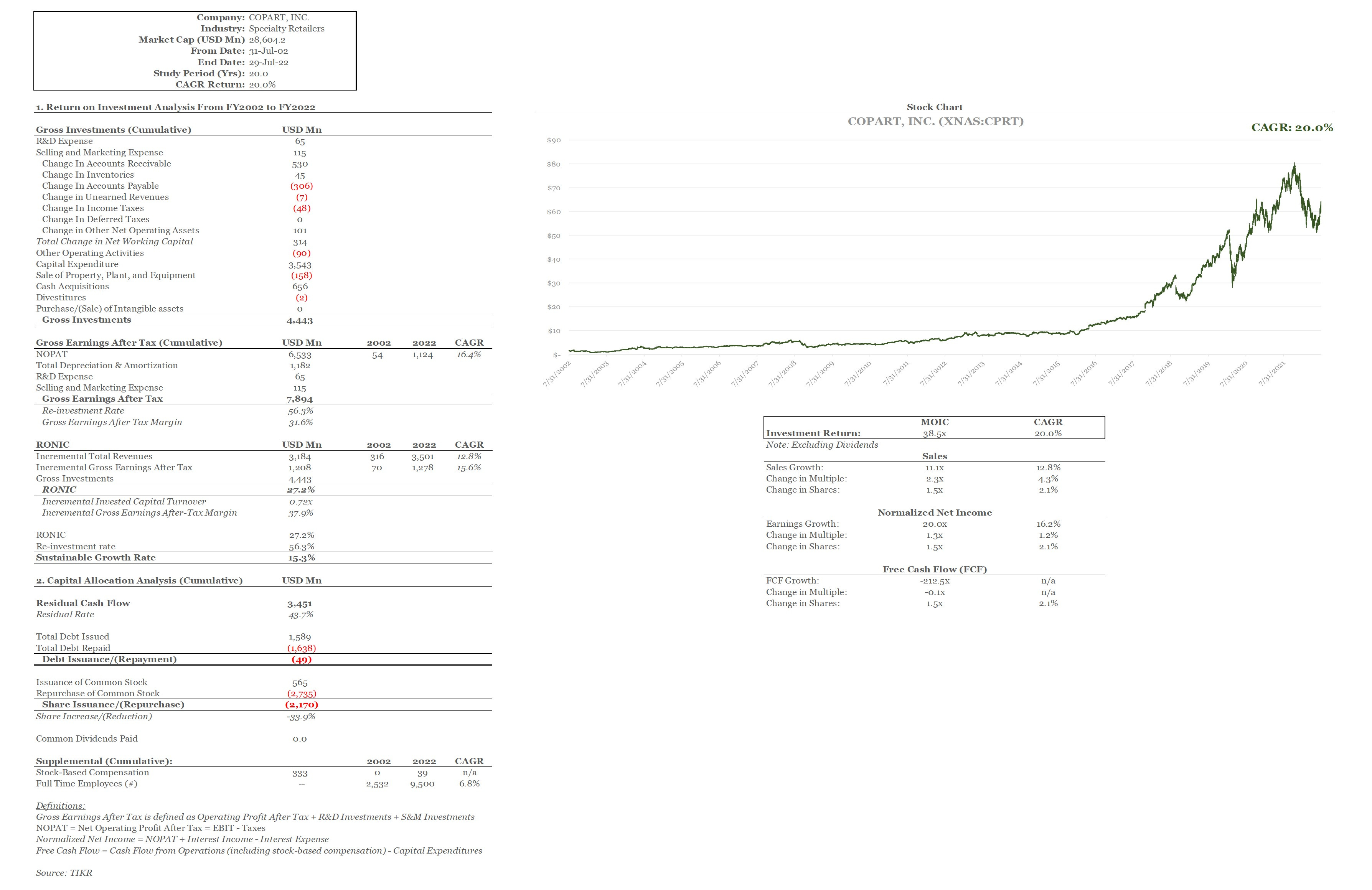

Overview

Founded in 1982 in Texas, Copart (CPRT) provides online auctions and vehicle remarketing services globally. The company has compounded shareholder value by more than 20% per annum over two decades between 2002 and 2022 not only through profitable reinvestment but also through shareholder-accretive capital allocation.

Return on Investment Analysis

Since 2002, CPRT has generated cumulative gross earnings of $7.9 Bn, of which the company reinvested approximately 56% ($4.4 Bn) primarily through its internally generated funds.

Out of the $7.9 Bn gross investments, $3.5 Bn was in the form of capital expenditures, mainly to own its land, and $0.7 Bn in cash acquisitions, with minimal net working capital requirements, speaking for a strong cash conversion cycle.

Altogether, these investments, alongside the initial capital in the business of course, have generated $3.2 Bn in incremental revenues, growing revenues at 12.8% CAGR, and $1.2 Bn in incremental gross earnings after tax (15.6% CAGR), for an incremental invested capital turnover of 0.72x at a gross earnings margin of 38%; the company has efficiently increased its gross margins as well as operating profit margins over time, enjoying strong operating leverage and a relatively fixed cost base (allowed faster cashflow/earnings growth than sales growth).

The resultant gross RONIC is 27.2%; for every dollar invested since 2002, the company has achieved 27.2%, making economically profitable investments.

Capital Allocation Analysis

The Company was able to generate mid-double digit growth rates over two decades while only reinvesting 56% of its gross cashflow. With the remaining 44%, the company utilized value-accretive capital allocation through share buybacks by retiring a cumulative 34% of share count, increasing the ownership of shareholders in the company. Buying back shares instead of paying dividends, given the tax inefficiency, is definitely a sound strategy.

Return Attribution

The company has compounded shareholder value at 20% per annum over the Study Period, generating a total of 38.5x return for shareholders. The company created the majority of its return (20x) from normalized net income growth, followed by 1.5x from share buybacks and only 1.3x return from multiple expansion.

Given the heavy-CAPEX nature of the business, FCF started negative in 2002 but became positive in 2003 and grew significantly over time. However, the company continues to invest heavily for the future.

"Remember cash is a fact, profit is an opinion."

Alfred Rappaport